Highlights:

|

The nation’s eyes remain fixed on the COVID-19 pandemic and the effect it continues to have on our healthcare system; naturally, COVID-specific metrics like case rate, ICU capacity, and vaccination uptake have dominated the conversation. “When will this be over?” is the question du jour. Unfortunately, emerging trends in the utilization of non-COVID-related healthcare services are leading health plans, physicians, and researchers to ask another question–“What happens to the preventative and elective care postponed during the pandemic’s height?”

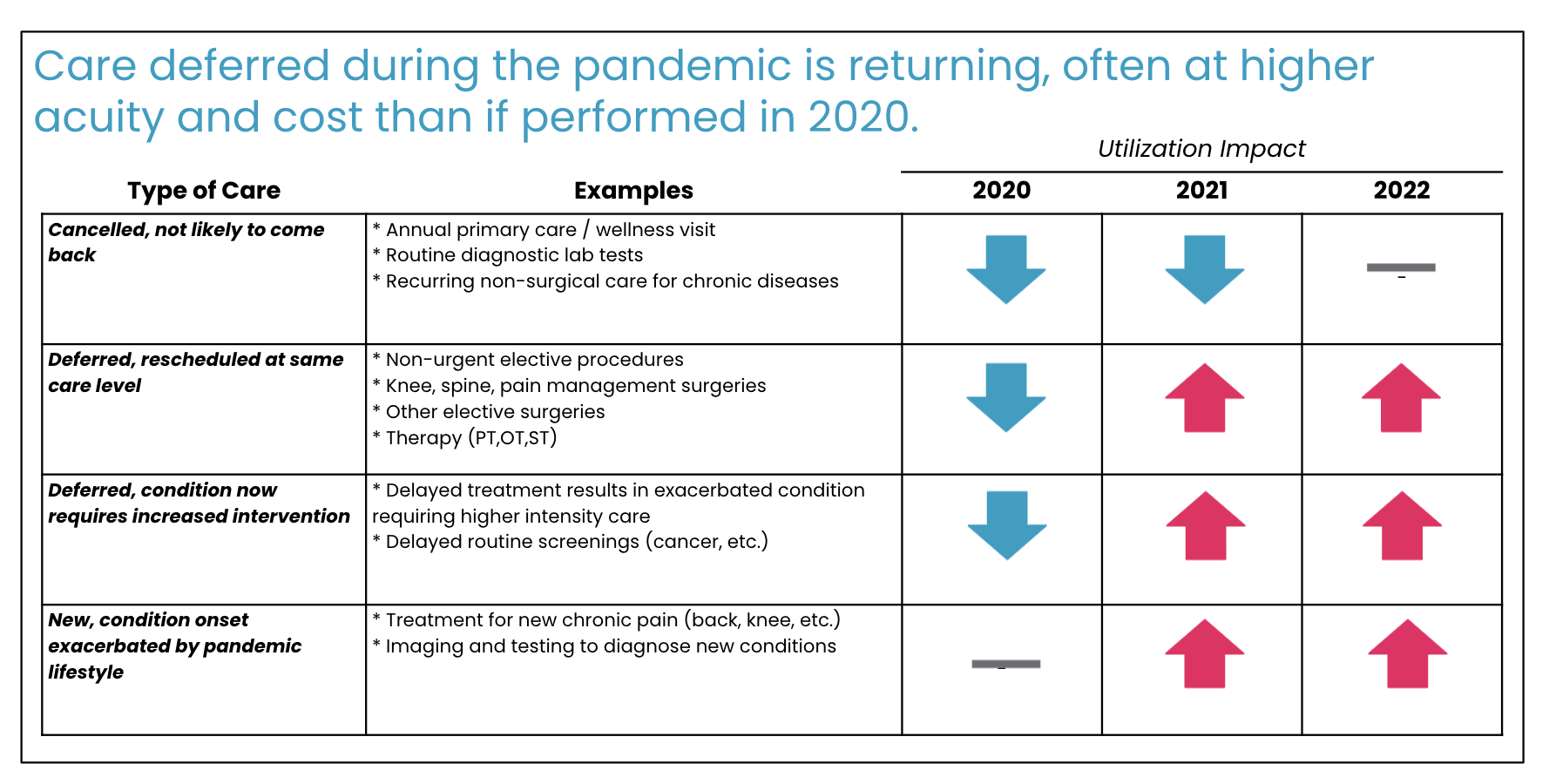

The answer is not yet clear, but early signals indicate that Americans have dramatically changed their consumption of healthcare services. Most experts believe the postponement of preventative care, routine diagnostic screenings, and canceled elective procedures at the pandemic’s height will have short and long-term consequences. However, the less obvious changes are how, where, and from whom patients seek out their care. Since spring of this year, a number of orthopedic, spine care, pain management, and physical therapy/rehabilitation services are experiencing a tidal wave of utilization. Why? Pent-up demand and growing supply. Specifically, a resurgence of patient demand while reopening and newly available supply comes online to meet that demand (i.e., reopening physician offices, newly built outpatient surgical facility/ASC capacity, and rescinded bans on inpatient elective procedures).

How do we know this is occurring?

For one, we can consider the backlog of routine procedures deferred at the onset of the pandemic last year. 2020 was the year of underutilization, with the occurrence of musculoskeletal procedures lagging well below those of previous years and the ensuing backlog estimated at one million spine and joint surgeries. This figure, as overwhelming as it already seems, carries a compounding effect with it: some patients’ conditions will have worsened in the waiting period for their procedure. The pandemic stokes the new onset or aggravation of certain risk factors and promotion of sedentary lifestyles. Additionally, the worsening of comorbidities like depression (which a stunning 90% of patients with Axial pain report experiencing), alcohol dependence, and increased nicotine use can intensify musculoskeletal problems, including neck and back pain. Our physicians are seeing these lifestyle trends with their patients as well. One of Cohere’s Associate Medical Directors for Primary Care and a practicing PCP, Mary Krebs, M.D., is seeing this with her patients. Dr. Krebs notes, “I would expect that worsening mental health would lead to higher costs in many areas, including musculoskeletal care. Depression and anxiety can amplify pain and may lead to nicotine or alcohol dependence. These factors can increase spending.”

When medical facilities moved out of crisis mode this year, we saw a preview of post-pandemic utilization. As physicians worked through the backlog of surgeries, Cohere found the number of Medicare patients seeking care for musculoskeletal problems in 2021 increased by 16%. This was a steep rise from the 3% annual growth documented prior to the pandemic. Specifically, we witnessed an increase in demand for Medial Branch Block injections, which are commonly used as diagnostic injections. This suggests that many patients are experiencing a new onset of symptoms and therefore only beginning their care journeys – more treatments are likely to follow.

A key trend running parallel to the jump in utilization is the increasing supply of Ambulatory Surgical Centers (ASC) which creates additional capacity for these surgeries to take place. ASCs are an attractive option for hospital-hesitant patients looking for safer, less costly treatment environments and they have earned the favor of regulatory entities and private health plans over the last few years. With ASCs becoming the primary setting for orthopedic procedures and CMS encouraging the flow of patients out of acute care hospitals, we can’t expect the wave of utilization to be stifled by limited hospital beds. The ASC has played a crucial role in allowing higher rates of utilization to flourish.

Endless as it seems, the pandemic will subside, but the orthopedics world will remain changed. The bar has been raised. COVID is testing us with a new level of need and accelerating already-present trends as we rise to meet it: plans will be tasked with handling higher volumes of claims while physicians and patients adjust to the outpatient model. Modifying our approach to this trend now could very well mean modifying it for the foreseeable future.

Special thanks to the Clinical Program, Quality and Trend Team for their constant work on identifying and assessing these patterns.